India-UK FTA: Insights from global FTAs & projected T&A export surge

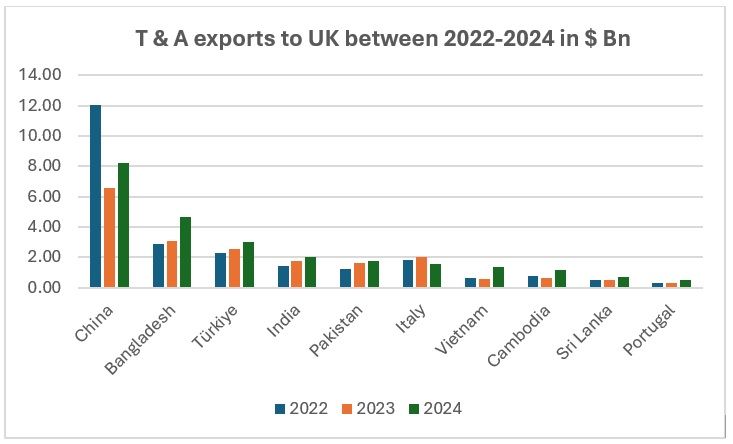

Exhibit 1

Source: TexPro

Competitive position: India vs. other top exporting countries

Once the UK-India FTA enters into force, India is expected to gain a significant competitive edge in the UK market through zero tariffs, improving its position relative to key apparel exporters:

- China remains the UK’s top supplier (~$5 billion, 25% share) but continues to face 12 per cent tariffs. The FTA gives India a cost advantage, making it a preferred alternative for price-sensitive UK buyers amid the ongoing ‘China+1’ sourcing shift. While China’s dominance will persist short term, India is likely to erode its share gradually.

- Bangladesh, the second largest supplier (~$4.6 billion), already enjoys duty-free access and lower labour costs. However, India now matches it on tariffs and can compete through a broader product range, faster scalability, and fewer capacity bottlenecks. The value gap is expected to narrow significantly by 2026.

- Türkiye currently ranks third but is expected to be overtaken by India by 2025-26, as Türkiye’s exports grow slowly and India’s tariff-driven momentum lifts its UK market share beyond Türkiye’s ~$3 billion level.

- Vietnam, Cambodia, Sri Lanka, and Pakistan benefit from FTAs or GSP+ but remain smaller players. India’s higher capacity and stronger product diversity will help it pull ahead of this group, becoming a clear third pillar alongside China and Bangladesh.

- Beyond tariffs, India’s advantages lie in its raw material base, skilled workforce, and value-added offerings. The FTA is also likely to trigger new investments and faster production turnaround, improving India’s long-term appeal to UK retailers.

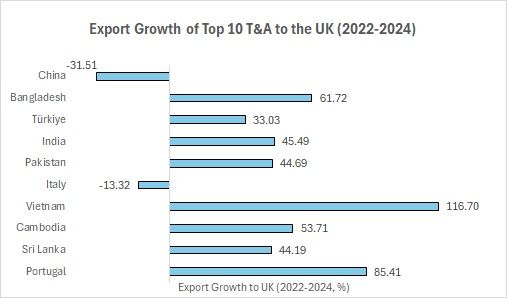

Exhibit 2

Source: TexPro

In terms of export growth (in per cent) of the top 10 textile exporters to the UK (2022-2024):

- Vietnam, Morocco, Portugal, Bangladesh, and Cambodia saw the strongest growth.

- India posted a solid +45 per cent, ahead of Türkiye and Pakistan.

- China and Italy showed declines, highlighting sourcing shifts.

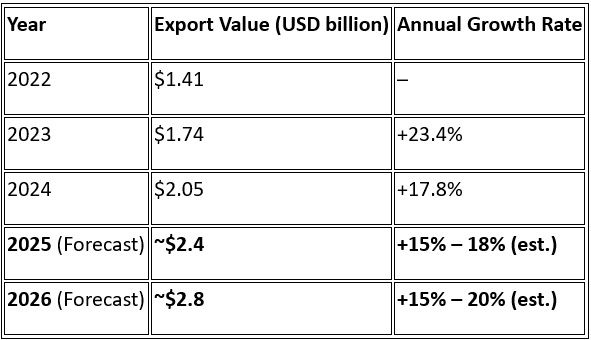

Table 1: India’s T&A Exports to the UK – Actual and Projected (USD billion)

Sources: Ministry of Commerce & Industry data (2022–24); projections for 2025–26 assume FTA-driven acceleration.

India-UK FTA: A turning point for Indian textile & apparel exports

Table 1 illustrates the anticipated boost in India’s textile and apparel (T&A) exports to the UK following the implementation of the Free Trade Agreement (FTA). Having reached $2.05 billion in 2024, exports are projected to grow at a robust 15-20 per cent annually, reaching approximately $2.4 billion in 2025 and $2.8 billion by 2026. This outlook is supported by strong industry momentum and consistent trends observed in other post-FTA trade environments.

Between 2022 and 2024, even before the FTA came into force, India’s exports to the UK grew at an impressive average annual rate of ~20 per cent, reflecting rising demand and improving price competitiveness. With the FTA now in place, this growth is expected to accelerate further, driven by tariff elimination, enhanced market access, and growing buyer confidence.

By 2026, India is forecast to become the third-largest T&A exporter to the UK, capturing a 10-12 per cent market share, up from approximately 6 per cent in 2023. This shift signals a significant realignment in UK sourcing patterns, positioning India as a central player in the post-FTA trade landscape.

Impact of the FTA: Tariff elimination and market access

The UK-India FTA eliminates tariffs on nearly 99 per cent of Indian textile and apparel exports, ending the 8-12 per cent import duties that previously limited India’s competitiveness. With this move, Indian products gain duty-free parity with key rivals such as Bangladesh and Vietnam, and a ~12 per cent cost advantage over Chinese suppliers, who still face standard MFN tariffs in the UK.

Key immediate effects:

- Cost Advantage: Indian exporters can now offer UK buyers ~10 per cent lower prices or retain higher margins, significantly enhancing competitiveness.

- Improved Market Access: Streamlined customs processes and mutual recognition of standards reduce non-tariff barriers, enabling broader and faster entry, especially for small and medium-sized exporters.

- Demand Surge: The UK’s apparel import market, valued at approximately $20 billion annually, presents a substantial opportunity. With UK buyers already increasing orders from India in late 2024 in anticipation of the FTA, demand is expected to accelerate in 2025–26.

In essence, the FTA removes India’s largest structural barrier—tariffs—placing it on equal footing with top competitors and unlocking new growth potential.

Expected changes in market share and rankings (2025-26)

The FTA is expected to significantly enhance India’s standing among textile and apparel exporters to the UK:

- Market Share: India’s share of UK imports could rise to 10-12 per cent by 2026, up from ~6 per cent in 2023. This growth reflects increased competitiveness and buyer confidence and could result in India doubling its share within two years.

- Ranking Shift: India is on track to become the third-largest supplier to the UK by 2025, overtaking Türkiye. If exports reach $2.8-3.0 billion by 2026, India will substantially narrow the gap with Bangladesh (~$4.5 billion) and set the stage for a potential contest for the #2 position in the longer term.

- Product Segment Leadership: Key gains are expected in ready-made garments, home textiles, and made-ups—categories previously impacted by high tariffs. India could rise to second place in specific niches such as women’s cotton apparel and home furnishings.

- Retailer Dynamics: Major UK retailers—such as Marks & Spencer, Tesco, and Primark—are likely to expand sourcing from India, capitalising on the cost savings and diversified product offerings enabled by the FTA. India is well-positioned to grow in both high-volume basics and premium, value-added segments.

Thus, the UK-India FTA represents a strategic inflection point for India’s textile and apparel exports. By eliminating tariffs and improving access to a $20 billion market, it empowers Indian exporters to grow market share, secure stronger buyer relationships, and reshape UK sourcing dynamics. By 2026, India is set to become one of the top three suppliers to the UK, with sustained momentum driving long-term trade expansion.

Insights from similar FTAs and trade preferences

Historical trade deals highlight how preferential access can drive export growth, supporting strong expectations for India post-FTA:

Bangladesh leveraged duty-free access under the EU’s EBA and UK’s GSP schemes to become a dominant apparel exporter to the UK, growing from $0.5 billion in 2001 to ~$5 billion by 2023. Its 12 per cent cost edge over India was a key factor. With the FTA removing this gap, India is now positioned to narrow the export lead, though Bangladesh will retain most of its duty-free status even post-LDC graduation.

Vietnam, under the UKVFTA since 2021, grew UK exports by ~9.4 per cent annually, even during global slowdowns. While its UK market share remains modest (~$0.7 billion), its experience shows that even in flat markets, FTAs support consistent growth. India, with a larger base, could grow faster under similar conditions.

Türkiye enjoys duty-free access via the UK-EU customs union and the UK-Türkiye FTA. Despite proximity advantages, its UK export growth has plateaued (~$2 billion, ~10 per cent share). India’s tariff parity and larger capacity puts it in a strong position to outpace Türkiye by 2026.

Other developing countries like Cambodia (EBA) and Pakistan (GSP+) have also benefited from reduced tariffs. These cases confirm that zero-duty access consistently enhances UK market presence. India, having lacked such access until now, is poised to catch up rapidly.

In essence, past FTAs show that tariff elimination fuels export growth, even in stable or competitive markets. So, once the UK-India FTA is implemented, India is expected to see a significant rise in apparel exports by 2025-26, following patterns similar to other nations discussed above.

Conclusion

The UK-India Free Trade Agreement is set to significantly boost India’s textile and apparel exports to the UK in the next 1-2 years. Fibre2Fashion projects India’s T&A exports to reach roughly $2.4 billion in 2025 and $2.8-3.0 billion in 2026, implying vigorous annual growth of 15 to 20 per cent or more. These forecasts are supported by historical parallels (other FTAs and preference schemes that drove export surges) and by industry optimism on the ground. Indian exporters will benefit from zero tariffs, improved market access, and a newfound cost advantage, enabling them to win a larger share of the UK’s ~$20 billion import market. By 2026, India will likely rise to become the third-largest supplier to the UK in this sector (up from fourth), narrowing the gap with Bangladesh (#2) and China (#1).

Fibre2Fashion News Desk (PN)