Colombo (LNW): Peoples Leasing has responded to certain Social Media allegations questioning the rationale for the investment decision to acquire First Capital Holdings PLC, with a comprehensive statement.

During a YouTube interview, several allegations were made by SJB analyst Niroshan Padukka against Peoples Leasing questioning the basis for acquiring 33% of shares of First Capital Holdings PLC.

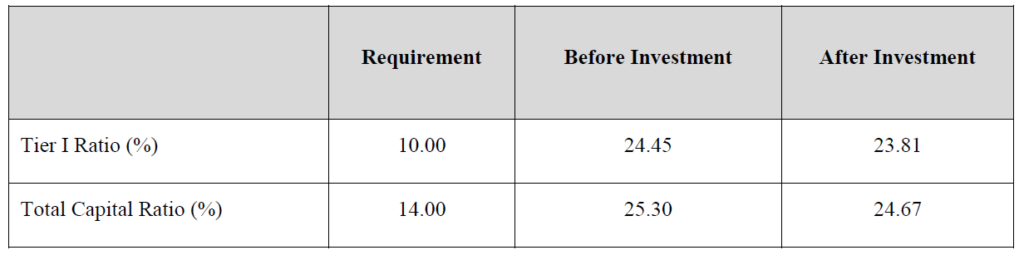

The company emphasised that PLC will continue to maintain strong capital ratios well above the externally imposed capital requirements, and even with an investment of Rs. 5 billion, post transaction the Total Capital Ratios are well above the regulatory capital adequacy ratio requirements.

Full Report: RATIONALE FOR THE INVESTMENT DECISION BY PEOPLES LEASING TO ACQUIRE 33% FIRST CAPITAL HOLDINGS PLCBackground

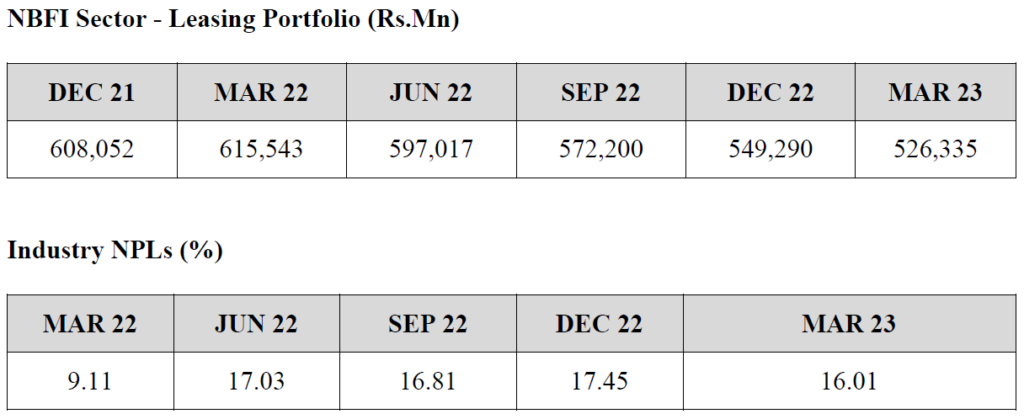

The NBFI sector has been one of the worst affected by the financial crisis and prior to that the COVID pandemic. NPL’s are at very high levels, the asset base is shrinking due to lack of new lending, collections are challenging and cash is building up which is difficult to deploy.

These factors have led to a decline in the NBFI sector’s attractiveness and a very low level of profitability.

In this environment, NBFI’s need to look at diversifying their risk and income streams. While the option of acquiring other NBFI’s is also available, this in no way diversifies the risk and return to PLC.

Hence, the need to look at opportunities in the broader financial services sector and the discussion with shareholders of First Capital Holdings PLC.

First Capital Holdings PLC (FCH)

FCH is the leading Non-Bank Primary Dealer in Sri Lanka, and also provides Unit Trusts, Private Wealth Management, Corporate Finance and Stock Brokering services.

It provides a set of complimentary financial services offerings to that of PLC, and numerous opportunities for synergies with the existing business operations of PLC.

FCH is regulated by the Securities & Exchange Commission (SEC) while its key subsidiary, FCT is related by both Central Bank of Sri Lanka (CBSL) and the SEC.

Company / Group performance

For the FY2022/23, the company and group reported a PAT of Rs 2.35Bn and Rs 2.6Bn respectively. Total assets grew by 60% and was reported at Rs. 66.67Bn.

Return on equity for the current financial year is 47.4%. This high ROE reflects efficient usage of shareholder funds and the benefit of the volatile interest rate environment.

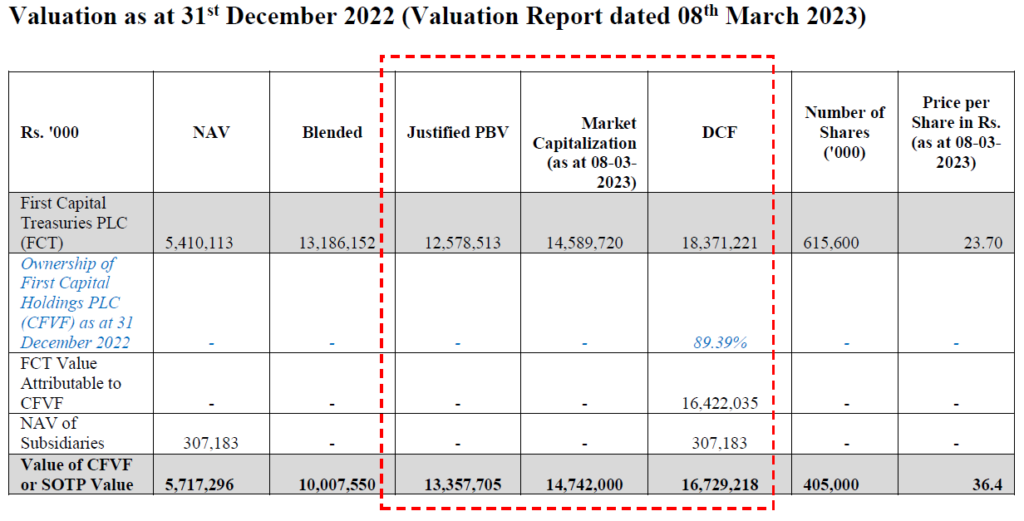

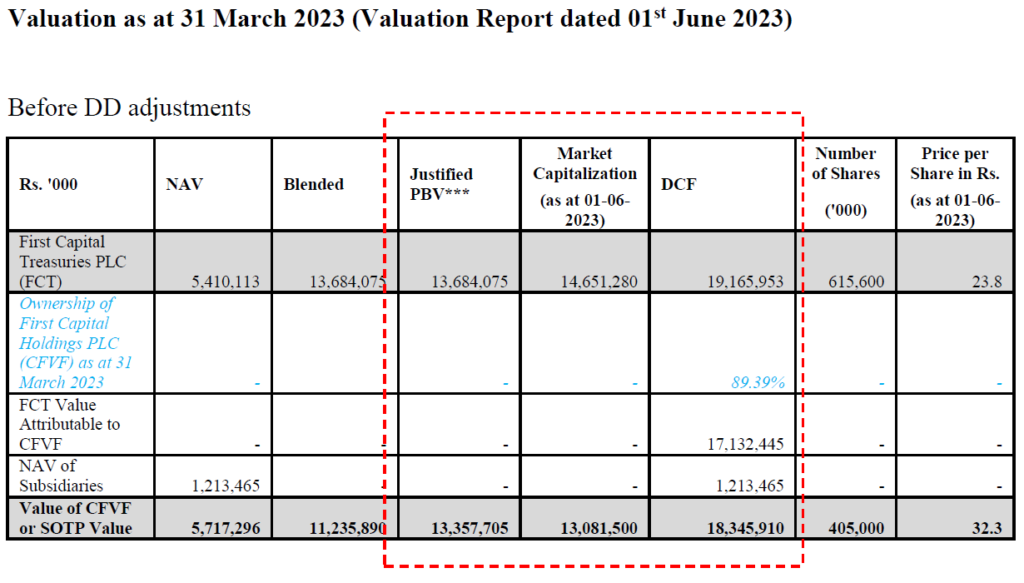

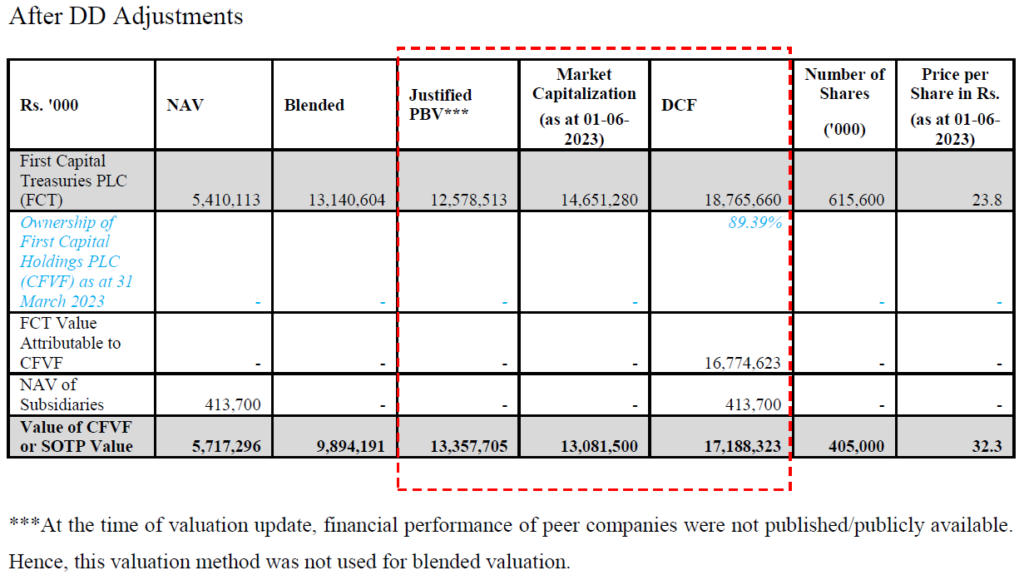

Valuation of First Capital Holdings (FCH)

The valuation for the purposes of the investment was done by the People’s Bank Investment Banking Unit (PBIBU).

The Seller’s deemed equity value for CFVF amounts to Rs.15Bn. The Expectation was within the Discounted Cash Flow (“DCF”) (based on a discount rate of 17% reflecting long term returns) value of the Group was not significantly above the market capitalization of FCH which ranged between circa. Rs. 13-14Bn, considering the strategic stake acquired. The DCF method was considered as the primary valuation method and is particularly relevant to a primary dealer type financial institution, as a primary dealer generates revenue primarily through its trading activities, commissions, fees and interest income. The high share price versus the NAV of the Company is a reflection of the high ROE’s generated by the business and the expectation of significant future profit from a declining interest rate environment.

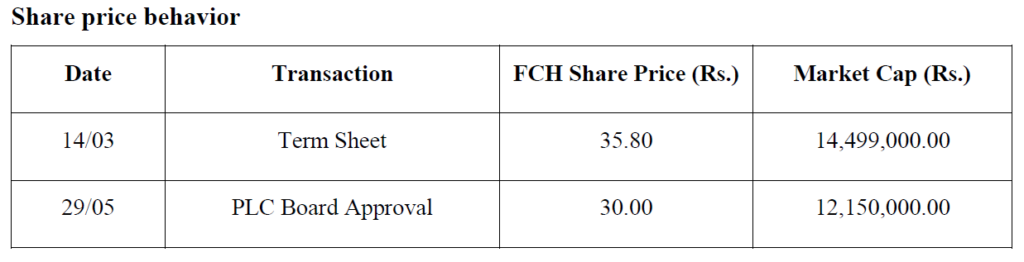

For the last one year period, the highest market cap recorded was Rs.16.6 bn for CFVF and the highest share price recorded was Rs. 41 on 23 January 2023.

Generally, for transactions with a significant stake being traded, a control premium of between 20-30% is expected on the pre-transaction price. In this event, the premium to the pre-announcement price was around 9%.

The Rs 37.10 offer price equates to a PE ratio of 6.4x, which is considered reasonable for a business that generated a Return on Equity of 47% on the average equity for the financial year FY22/23.

The recently announced sale of a 50.1% stake in Dankotuwa Porcelain was done at a premium of 14% to the pre-transaction price.

Transaction Details

PLC was advised by the PBIBU as the Lead Manager, by KPMG on the transaction process and project management, by the leading law firm Varners on all legal matters including the legal due diligence and Ernst & Young on the financial and tax due diligences.

With the sanction of the Board Investment Committee (BIC) and the Board of Directors (BOD), a detailed Term Sheet was signed between the parties, which gave a 90 day exclusivity period for PLC to carry out due diligence and execute the necessary legal documentation.

Potential Synergies of the proposed Acquisition

(a) PLC will be able to diversify its product and service offerings, which can lead to increased/diversified revenue and profit streams mainly stemming out from the FCH’s expertise in areas such as Investment Banking, Wealth Management, and Securities trading. Further, integrating these services into its own portfolio will enhance PLC’s competitive and financial position in the financial services industry.

(b) PLC is one of the largest non-banking financial institutions in the Country and has managed to secure market leadership in the leasing industry. With the proposed acquisition, PLC will be able to unlock many synergies that will strengthen its profitability and enhance its competitive position in the financial services industry.

(c) PLC’s current exposure to the margin trading business can be further expanded by partnering with the Stockbroking operations of FCH and achieving portfolio growth.

(d) There are also potential benefits stemming out from better management of treasury operations for both Companies, as the Corporate Finance arm of FCH can facilitate the funding requirements of PLC, while also enabling the company to better manage Asset and Liability mismatches. At the same time, any excess funds can be better managed to maximize returns while minimizing risk exposure through the expertise stemming from FCH’s PD and Asset Management business.

(e) Exploring the possibility of expanding the reach and expertise of FCH in investment banking and capital markets to Bangladesh through an alliance with Lankan Alliance Finance Limited (LAFL) held by PLC could potentially bring benefits to both entities, particularly in terms of access and entry to the frontier markets.

(f) Further this transaction will demonstrate as to how best private/public partnerships could enhance the business efficiencies and effectiveness. By working together, private and public entities can combine their resources, expertise, and networks to achieve common goals that benefit both parties.

Impact on PLC

PLC will continue to maintain strong capital ratios well above the externally imposed capital requirements, and even with an investment of Rs. 5 billion, post transaction the Total Capital Ratios are well above the regulatory capital adequacy ratio requirements.

PLC is not going to borrow to fund the transaction and will use existing excess liquidity investments to fund this transaction.